Medicare Advantage Denial Rates Are a Scandal

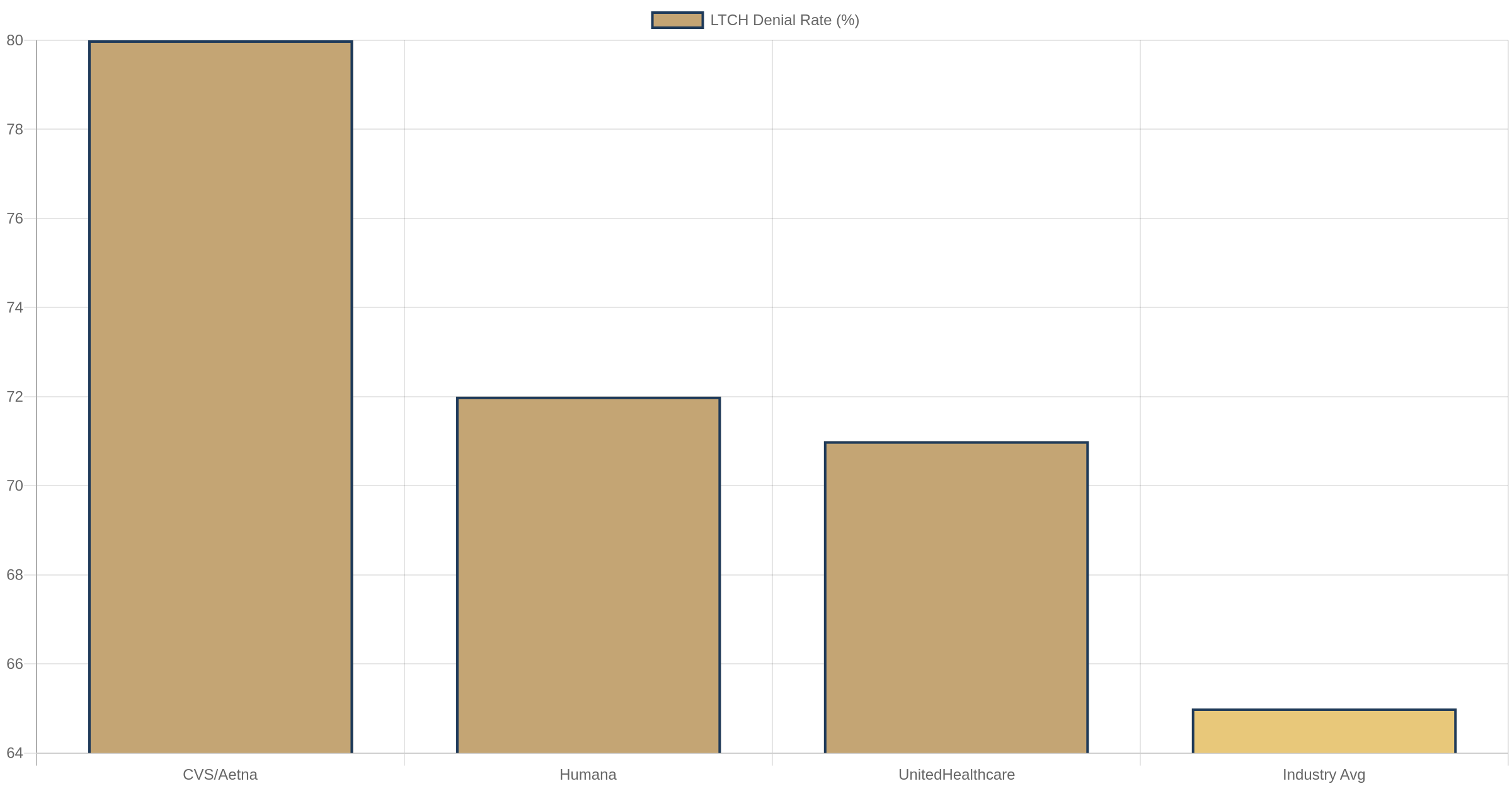

CVS denies 80% of long-term care claims. Humana denies 72%. United denies 71%. This isn't utilization management. It's a business model.

The Numbers Are Not in Dispute

Let's start with what we know, because the data is unusually clear.

In June 2026, the Office of Inspector General published two back-to-back reports on Medicare Advantage (MA) denial rates for post-acute care. These weren't advocacy pieces. They weren't patient complaints. They were federal audits of actual claims data from the 19 largest Medicare Advantage Organizations (MAOs), covering Long-Term Care Hospitals (LTCHs), Inpatient Rehabilitation Facilities (IRFs), and Skilled Nursing Facilities (SNFs).

Here's what they found:

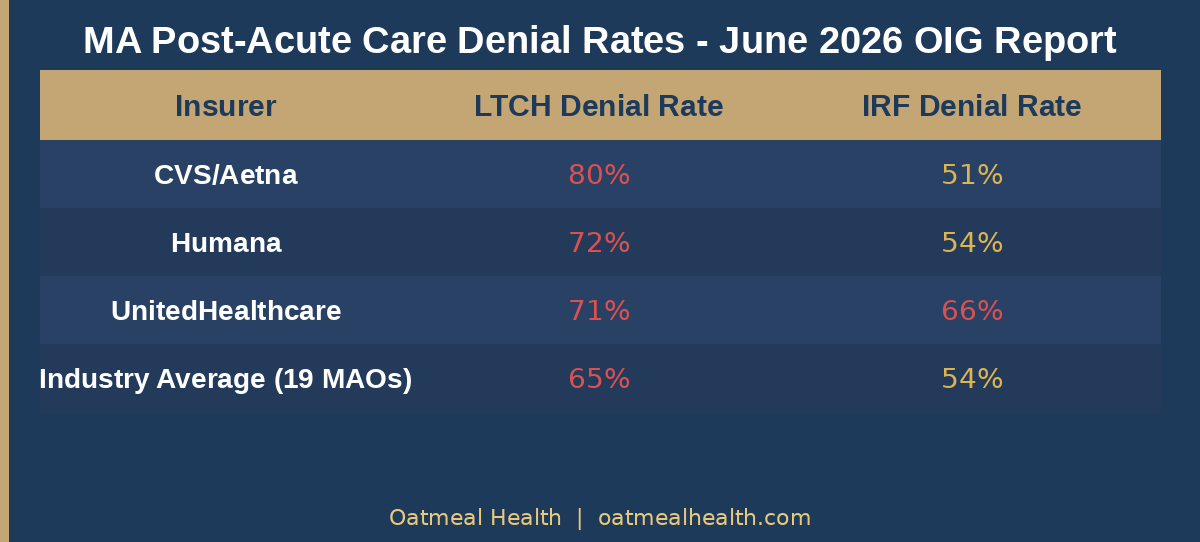

The 19 largest MAOs denied 65% of LTCH claims, 54% of IRF claims, and 12% of SNF claims. But the headline numbers obscure the individual insurer performance, which is where it gets damning.

CVS/Aetna denied 80% of LTCH claims and 51% of IRF claims. Humana denied 72% of LTCH claims and 54% of IRF claims. UnitedHealthcare denied 71% of LTCH claims and 66% of IRF claims.

These are not marginal facilities. Long-Term Care Hospitals serve patients recovering from catastrophic illness - strokes, traumatic injuries, ventilator dependence, complex wounds. Inpatient Rehabilitation Facilities treat patients after hip replacements, spinal injuries, and brain trauma. These patients need this care. Their physicians prescribed it. And at rates between 65% and 80%, the largest insurers in the country said no.

The Appeals Data Tells the Real Story

Here is the part the insurers would prefer you not think about too hard.

When patients and providers appeal these denials, they win - a lot. For LTCH denials, 36% are overturned on appeal. For IRF denials, 43% are overturned on appeal. For SNF denials, the number is extraordinary: 95% of appealed SNF denials are overturned.

Read that again. When SNF denials are appealed, providers win 95% of the time.

There are two ways to interpret this. Either the initial denial process is so broken that nearly every SNF denial is wrong, or the appeals process is broken in the other direction. Given that these are federal audits of actual outcomes, the former is far more likely.

What does it mean when you deny 12% of SNF claims and then lose 95% of the appeals? It means you're denying medically necessary care, getting caught, and reversing course - but only for the patients and families who have the time, knowledge, and energy to fight back. For everyone else, the denial sticks.

UnitedHealth's Algorithm Problem

The OIG reports specifically flagged a pattern worth understanding: contractor-driven denials that the MAOs themselves overturned on appeal. In plain English, insurance companies hired third-party contractors to make initial denial decisions using algorithms, and then those same insurance companies reversed the algorithmic decisions when humans reviewed them on appeal.

This is not a theoretical concern. The DOJ is currently investigating UnitedHealth Group for exactly this issue. UHC's denial rate went from 8.7% in 2019 to 22.7% in 2022 - a 161% increase - after the company acquired NaviHealth, a post-acute care management company that uses algorithmic prediction tools.

UHC's SNF denial rate went from 1.4% in 2019 to 12.6% in 2022 - a ninefold increase. In three years. After acquiring a predictive algorithm company.

The OIG's guidance in these reports was explicit: MAOs cannot rely solely on an algorithm without considering the member's specific circumstances. This is not just a best practice recommendation. It is a statement about what the law requires. The algorithm-only approach, which drove the post-NaviHealth denial surge, was illegal.

The DOJ investigation is not just civil. According to reporting in 2024 and 2025, UnitedHealth faces both civil and criminal exposure. The company's CEO was murdered in December 2024 - a national news event that briefly made the entire country aware of what the healthcare denial machine looks like from the outside.

This Is What $76 Billion in Overpayments Buys

Here is the full picture, because the denial story and the overpayment story are two sides of the same coin.

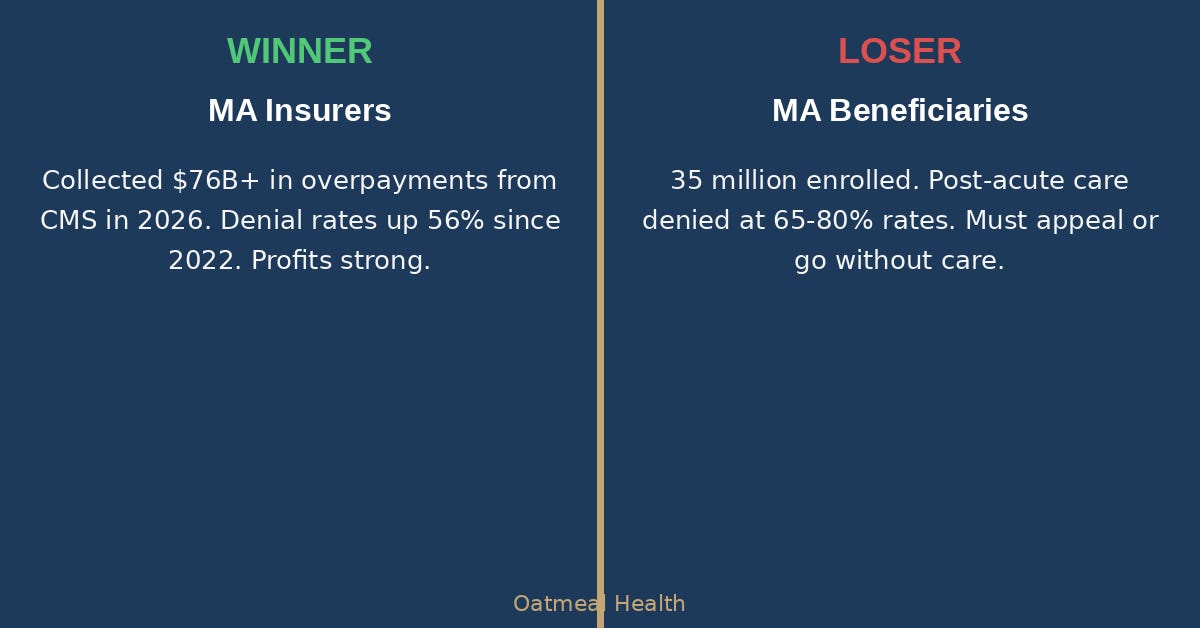

MedPAC - the independent Congressional advisory body on Medicare - estimates that MA plans will receive $76 billion in overpayments from CMS in 2026. That is $76 billion above what traditional Medicare would have cost for the same beneficiaries.

These overpayments come from two sources: favorable risk selection (enrolling healthier-than-average seniors) and upcoding (adding diagnosis codes to make patients look sicker than they are, which increases per-member payments). OIG found $462 million in overpayments on unsupported stroke diagnoses alone in 2021. Kaiser Permanente paid a $556 million DOJ settlement in January 2026 for unsupported diagnosis codes. Elevance paid $342 million to CMS in May 2026.

The business model works like this: collect more money by making patients look sicker on paper, then deny the care those patients actually need. The spread between inflated risk scores and actual care delivered is profit.

The scale is staggering. MA now covers 35 million Americans - 55% of all Medicare-eligible seniors, up from just 19% in 2007. The program grew by 1.1 million beneficiaries between 2025 and 2026 alone. Those overpayments are funded by all Medicare beneficiaries: they drove the Part B premium from $185 in 2025 to $203 in 2026. Every American on Medicare is paying higher premiums to fund a system that denies post-acute care to the sickest seniors at 80% rates.

CMS Is Watching But Not Acting

In April 2024, CMS finalized new prior authorization rules requiring MA plans to make expedited decisions within 72 hours and standard decisions within 7 calendar days. These are improvements. They don't take full effect until 2026.

In January 2027, MA plans will be required to implement HL7 FHIR-based Prior Authorization APIs - meaning electronic, real-time authorization requirements that providers can query directly. This is meaningful infrastructure change.

But in June 2025, CMS announced it will not enforce the utilization management health equity reporting rules it had previously established. The agency cited administrative burden. The rules would have required MA plans to report on whether their denial rates varied by race, income, and geography - data that might have revealed whether the 80% LTCH denial rate falls disproportionately on certain populations.

CMS suspended those transparency requirements right when they would have started to bite.

The enforcement picture is mixed at best. The DOJ is pursuing criminal and civil cases. CMS is requiring faster decision timelines. But the fundamental economics haven't changed. An MA insurer that denies 80% of LTCH claims and reverses 36% of those on appeal is still, on net, denying more than half of medically necessary LTCH placements. The math works in their favor as long as most patients don't appeal.

The Moral Hazard of Managed Medicare

I want to be precise about what I am and am not arguing here.

I am not arguing that utilization management is inherently wrong. Every insurer, including traditional Medicare through its MACs, reviews claims and denies some percentage of them. Some denials are appropriate. Prior authorization, when done well, can reduce unnecessary care and lower costs.

What I am arguing is that an 80% denial rate, combined with a 36% appeal overturn rate, is not utilization management. It is a business strategy.

Utilization management done correctly looks like: review the claim, verify medical necessity using evidence-based criteria, make a decision within 24-72 hours, approve most clinically appropriate care, deny a small percentage with strong clinical rationale, and lose very few appeals because your initial decisions were correct.

What CVS, Humana, and UnitedHealth appear to be doing looks like: deny by default using an algorithm, count on most patients not appealing, reverse denials when challenged, and treat the 36-43% overturn rate as an acceptable cost of doing business.

The difference matters enormously when you're talking about post-acute care. A stroke patient who needs inpatient rehab doesn't have weeks to wait for an appeal. A ventilator-dependent patient whose LTCH placement is denied doesn't have the bandwidth to navigate an administrative process while managing a life-threatening illness. A family dealing with a parent's hip fracture recovery doesn't know they have appeal rights, let alone how to exercise them.

Denial is most harmful when it falls on the most vulnerable patients, who are least able to fight back.

What Should Change

The OIG reports make specific recommendations. CMS should require MAOs to document why they denied claims and track denial rates by facility type. CMS should audit plans with outlier denial rates. Plans should not be allowed to use algorithm-only review without human clinical oversight.

These are the right recommendations. They are not sufficient.

What would actually move the needle:

First, minimum overturn rate triggers. Any MA plan with an appeals overturn rate above 30% in any post-acute care category should face automatic review and rate adjustments. You cannot lose 43% of your appeals and call that good-faith utilization management.

Second, denial rate benchmarks tied to traditional Medicare. CMS knows what traditional Medicare's denial rates are. MA plans should not be allowed to run denial rates more than two standard deviations above the traditional Medicare baseline for the same beneficiary risk categories.

Third, real-time adverse event tracking. When a patient is denied post-acute care and subsequently requires emergency readmission, that outcome should be automatically linked to the prior denial and flagged for review. MA plans should bear financial consequences for readmissions that follow denials of medically necessary post-acute care.

Fourth, eliminate the algorithm defense. Plans that use predictive tools for initial denial decisions should be held to the same standard as human reviewers. The OIG has already said plans cannot rely solely on algorithms. CMS should codify this as an enforceable standard with financial penalties.

The 35 Million Person Question

Medicare Advantage has genuinely delivered value in some areas. Care coordination, dental and vision benefits, wellness programs - these are real improvements over fee-for-service Medicare for many beneficiaries. The program is not without merit.

But merit in some areas does not offset systematic denial of medically necessary care in others. And the scale of MA - 55% of all Medicare beneficiaries, $400+ billion in federal spending annually - means that systematic problems in MA are systematically large problems.

Thirty-five million Americans chose Medicare Advantage because they were told it would offer better coverage and lower costs than traditional Medicare. Many of them will eventually need post-acute care. When they do, there is approximately a 65-80% chance, if they're in an LTCH or IRF, that their MA plan will say no.

The insurers know this. CMS knows this. The OIG has now documented it twice in a month. The DOJ is investigating the largest player.

The question is whether any of this produces actual change before another cohort of stroke patients and hip fracture survivors gets algorithmically denied into discharge destinations that compromise their recovery.

Based on the pace of federal enforcement in health insurance, I am not optimistic. The MA denial machine is profitable, entrenched, and protected by the same lobbying apparatus that keeps drug prices high and surprise billing alive. The OIG reports will generate congressional letters. The DOJ settlements will generate press releases. And on Monday morning, the algorithm will keep running.

That is the scandal. Not that it happened. That we have documented it thoroughly and are largely going to let it continue.

Oatmeal Health covers healthcare policy, payment reform, and the business of medicine. Sources for this piece include the OIG June 2026 reports on MA denial rates for LTCHs, IRFs, and SNFs; MedPAC March 2026 Report to Congress; KFF Medicare Advantage 2026 enrollment data; and prior reporting on UnitedHealth NaviHealth acquisition outcomes.