ACA Collapse Is a Systemic Failure

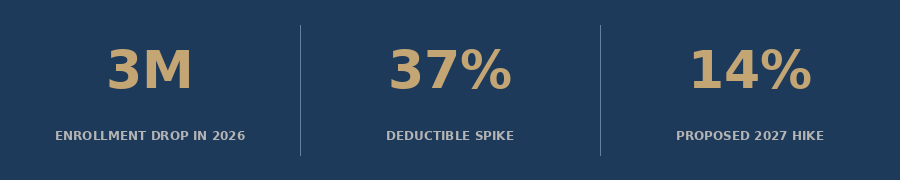

Three million Americans lost ACA marketplace coverage in 2026, deductibles hit a record $3,786, and insurers are already filing 14% hikes for 2027 - this is not a fraud story, it is a pricing-out story.

The official story coming out of Washington is that ACA marketplace enrollment fell in 2026 because the government cracked down on fraud. Tens of thousands of people were enrolled without their knowledge, the argument goes, and now that the rolls have been cleaned up, the numbers look smaller.

That framing is politically convenient. It is also wrong.

The real story is simpler and more damaging: Congress allowed the enhanced premium tax credits to expire at the end of 2025, premiums roughly doubled for millions of enrollees, and people stopped buying coverage they could no longer afford. The market did exactly what markets do when prices spike without warning. People left.

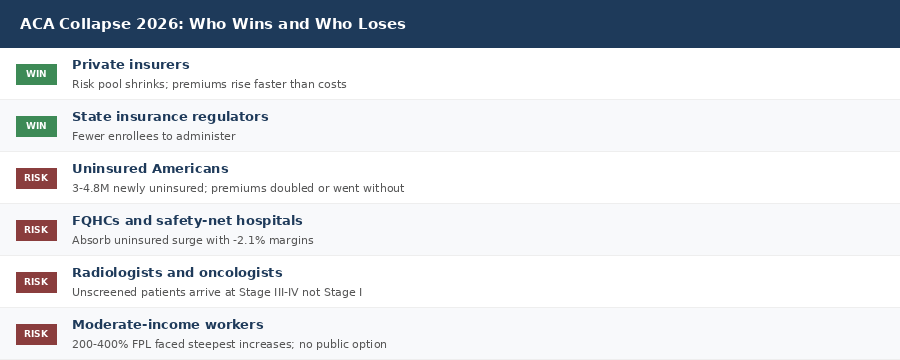

What we are watching is not a fraud cleanup. It is a coverage collapse in real time. And the institutions that will absorb the fallout - FQHCs, safety-net hospitals, community health centers - are already operating in the red.

1. The Numbers Behind the Collapse

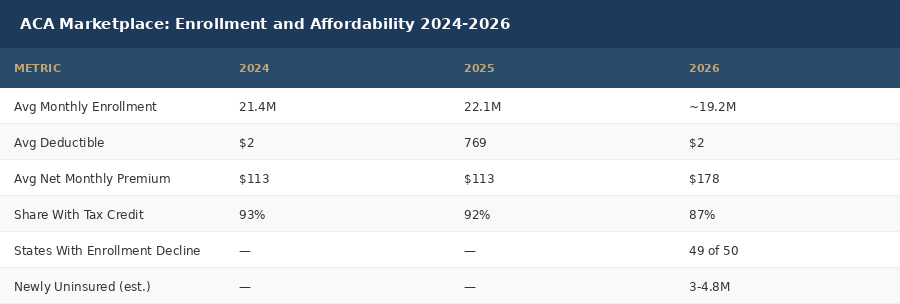

Start with what actually happened. ACA marketplace enrollment fell from 22.1 million at the end of 2025 to 19.2 million in February 2026 - a drop of roughly 3 million people, or 13 percent, in a single enrollment cycle. That is the steepest single-year decline since the ACA marketplaces were created. It is not a rounding error.

The drop was not evenly distributed. Forty-nine of fifty states and Washington, D.C. saw enrollment fall. Ohio, Oklahoma, and Arizona each shed roughly 30 percent of their enrolled population. New Mexico was the only exception, posting a 14 percent gain. The pattern is unmistakable: states with fewer backup coverage options and weaker state-level subsidy programs took the hardest hits.

📊 Average marketplace deductibles surged 37% to a record $3,786 in 2026 - the largest single-year deductible increase in the program's history (KFF).

The average deductible increase tells you something important about who stayed in the market. Healthier, wealthier enrollees who had options simply left. The people who stayed were disproportionately those who could not afford to go uninsured - people with chronic conditions, ongoing prescriptions, or complex care needs. The risk pool got sicker. Insurers responded by pricing up. And the cycle began.

The KFF deductible analysis is striking: the average marketplace deductible grew by $1,027 per person in a single year, landing at $3,786. This is the largest deductible increase in marketplace history. Many of these enrollees also shifted from silver plans (which had cost-sharing reductions under the enhanced subsidy regime) to bronze plans with high deductibles and minimal benefits. They stayed enrolled on paper. They stopped being able to use their coverage in practice.

A KFF survey fielded in late February and early March 2026 found that 9 percent of 2025 marketplace enrollees had become uninsured by early 2026. That is one in eleven people who had coverage last year and do not have it today.

2. The Fraud Framing Is a Political Escape Hatch

The Trump administration has pointed to a cleanup of fraudulent ACA enrollments as the primary driver of the 2026 decline. The claim goes that bad actors were signing people up for coverage without their knowledge under the Biden-era enhanced subsidy regime, and that tightened verification has corrected the rolls.

There is a kernel of truth buried in this. CMS did crack down on broker fraud in 2025, and some enrollments that were fraudulent or erroneous were removed. That is legitimate and appropriate.

But it does not explain what happened. Enrollment did not fall because a cleanup removed phantom enrollees. Enrollment fell because real people did the math and could not make it work.

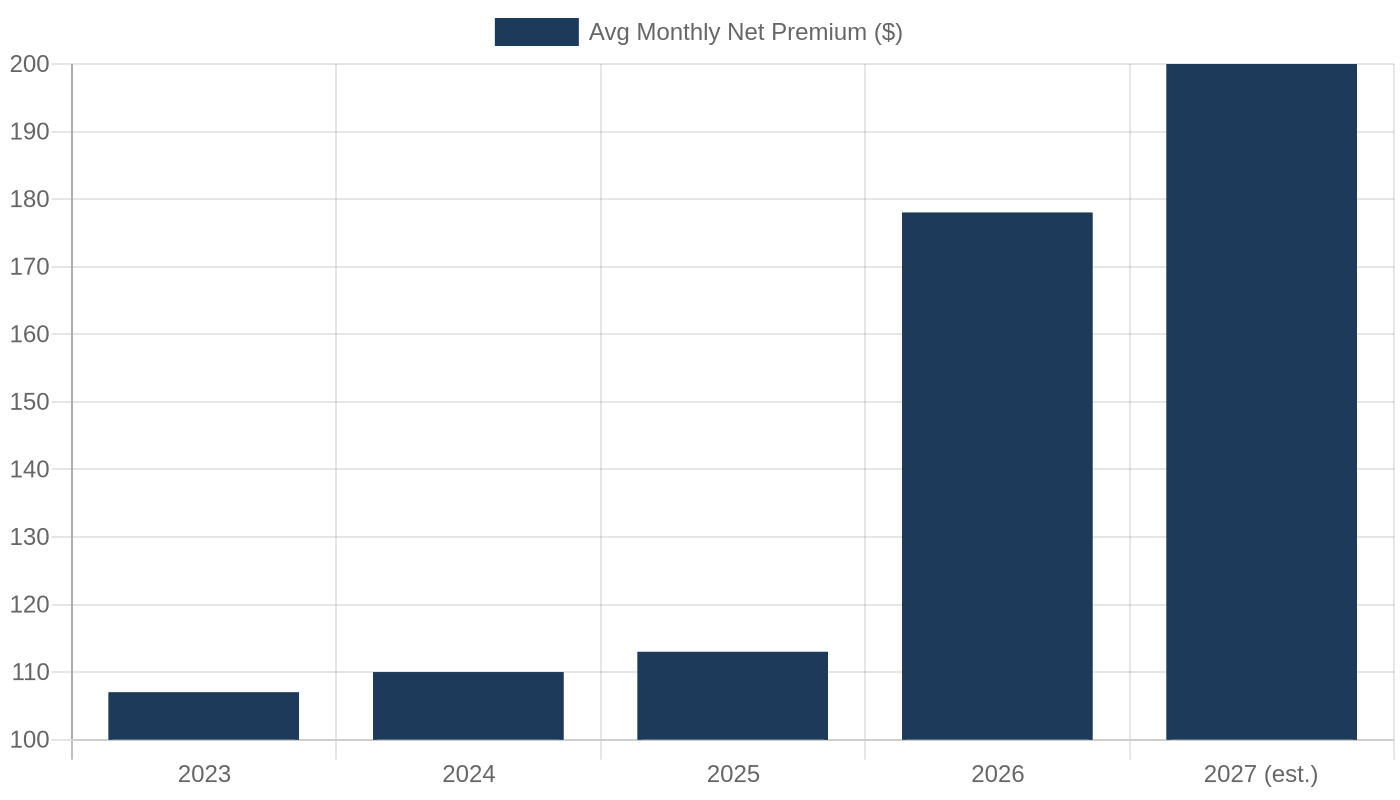

📊 The average monthly net premium for subsidized ACA enrollees rose 58% from $113 to $178 in 2026 - and that is after tax credits. Without enhanced subsidies, some enrollees saw premium payments increase by 114% to keep the same plan (KFF analysis).

Consider the mechanism. The enhanced premium tax credits that expired at the end of 2025 had capped premium contributions at 8.5 percent of income for all income levels and made plans free or nearly free for enrollees below 150 percent of the federal poverty level. When those credits expired, the price of coverage reverted to what it had been before - which, for many people at moderate income levels, meant a premium increase of hundreds of dollars per month.

People at the margin of affordability - those at 200 to 400 percent of the federal poverty level who were not getting the richest subsidies - found themselves priced out entirely. The consumers with incomes above the subsidy cliff (above 400 percent FPL) made up just 7 percent of 2025 enrollment but accounted for nearly 48 percent of the enrollment decline. This is not fraud cleanup. This is price sensitivity behaving exactly as economists would predict.

When a product doubles in price and demand falls, we do not call that a demand-side failure. We call it a pricing problem.

3. The Premium Spiral: 2026 Was Bad. 2027 Will Be Worse.

Here is the part that should alarm every health system leader and FQHC administrator reading this: the dynamic that caused 2026's coverage losses has not been corrected. It has been compounded.

Insurers are now filing preliminary rate requests for 2027 ACA marketplace plans. The median proposed increase across 77 insurers in 16 states and Washington, D.C. is 14 percent. Twenty of those insurers are requesting increases above 20 percent. The July 15, 2026 filing deadline has already passed for most states, and the early picture is a second consecutive year of double-digit premium increases.

Why are rates rising again when enrollment already fell sharply? Because of the risk pool problem.

When healthier, wealthier people exit a risk pool, the remaining enrollees are on average sicker and more expensive to cover. Insurers adjust for this by raising premiums. But higher premiums price out more healthy people at the margin, making the remaining pool sicker still. This is the adverse selection spiral that health economists have warned about since the ACA was designed. It is now happening in real time.

📊 Insurers cite the expiration of enhanced tax credits, a deteriorated risk pool (adding an estimated 4 percentage points to 2026 rates), rising GLP-1 costs, and healthcare inflation as drivers of 14% median proposed 2027 premium increases (KFF).

The spiral has a floor, but it is an ugly one: a market of primarily high-cost enrollees with very high premiums and minimal enrollment. This is what happened to individual insurance markets before the ACA existed in many states. We called it a market failure then. We are rebuilding it now with different branding.

4. Who Gets Left Behind: The FQHC Crisis

For radiologists, pulmonologists, and health system administrators, this might sound like a marketplace policy problem - important but distant. It is not. The people leaving the ACA marketplace do not disappear. They show up in your emergency department. They show up at FQHCs. They show up later, sicker, and harder to treat.

FQHCs are required by law to serve all patients regardless of ability to pay. They are the floor of the safety net. And right now, the floor is cracking.

KFF data shows that health center net margins fell from 1.6 percent in 2023 to negative 2.1 percent in 2024 - before the ACA coverage losses fully hit. NACHC projects that up to 5.6 million FQHC patients could lose coverage as a result of the combined impact of ACA subsidy expiration and Medicaid work requirements. Federal grant dollars for FQHCs remained essentially flat from 2019 to 2023 while healthcare costs rose more than 25 percent.

The math is straightforward and brutal: more uninsured patients, less reimbursement per patient, flat grant funding, and deteriorating margins. That is not a sustainability challenge. That is a closure sequence.

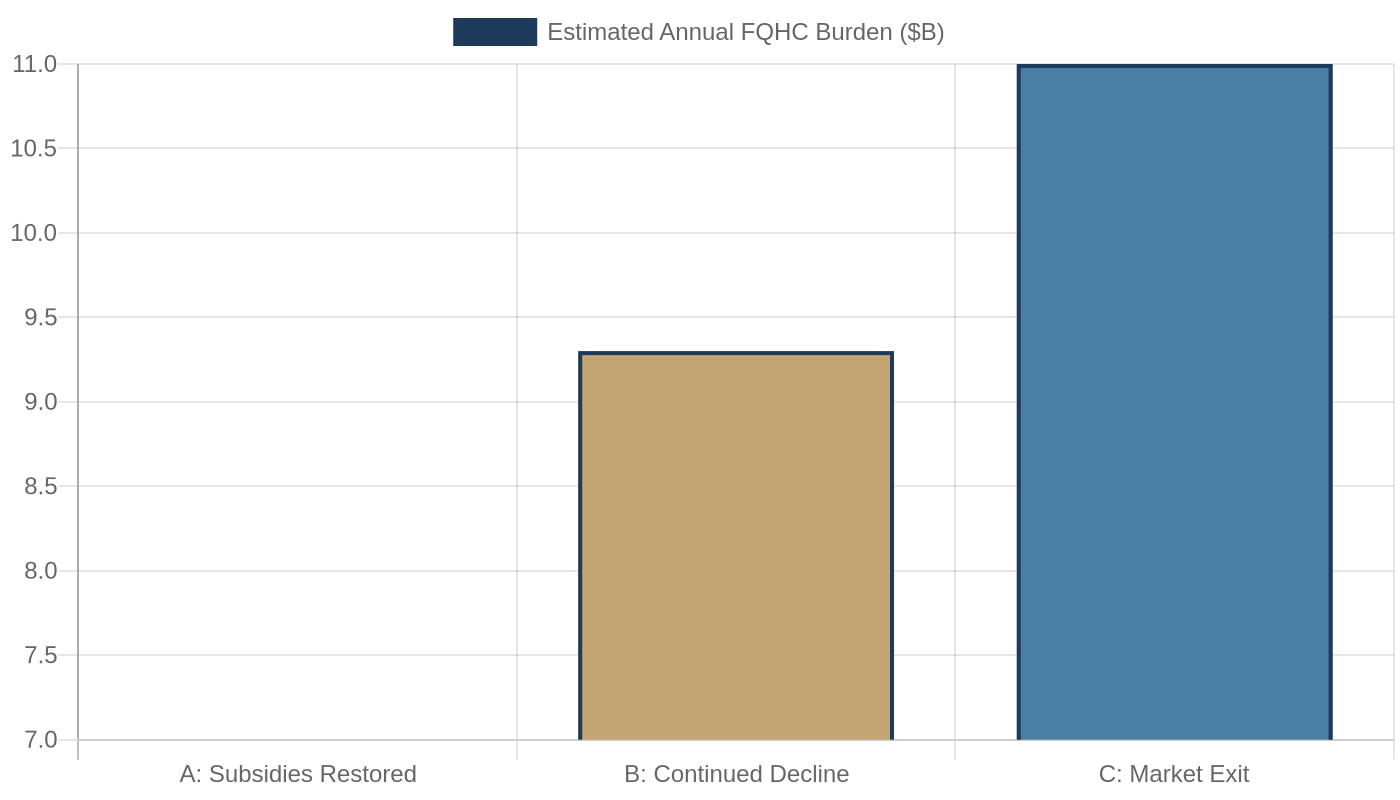

📊 NACHC projects up to 5.6 million FQHC patients could lose coverage. Health center net margins fell to -2.1% in 2024 - before ACA losses fully hit.

For radiologists and pulmonologists specifically: FQHC patients are the highest-risk population for lung cancer. They are the people who smoked for 30 years working jobs without health benefits. They are the people who never got a screening CT because no one navigated them to one. When FQHCs lose capacity - when they cut care coordinators, reduce imaging access, or close sites - these patients fall through entirely. The gap between Stage I survival (77 percent) and Stage IV survival (9 percent) is not a clinical gap. It is an access gap. And every percentage point of FQHC margin erosion widens it.

5. Deep Dive: The Scenario Model

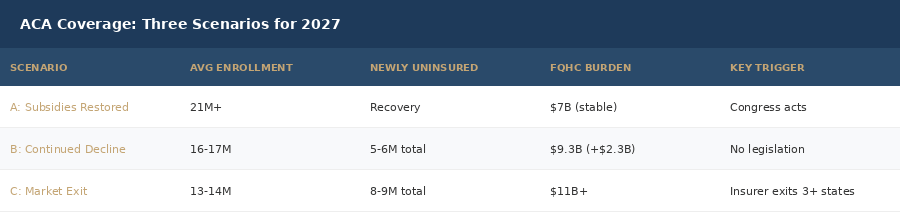

The coverage cliff does not have a single landing point. It plays out differently depending on what Congress does in the next 12 months. Here are the three scenarios that health system planners and FQHC administrators should be modeling right now.

Scenario A: Subsidies Restored Before 2027 Open Enrollment

If Congress acts in the next legislative window to restore some version of the enhanced premium tax credits, the adverse selection spiral can be interrupted. Healthy enrollees return, risk pools stabilize, and 2027 rate increases moderate.

This is the best-case outcome. It is also the least likely given the current congressional composition and the absence of any serious legislative vehicle for ACA restoration. The enhanced subsidies that expired were themselves an extension of a temporary provision from the Inflation Reduction Act. Restoring them requires 60 Senate votes or reconciliation room that does not currently exist.

Scenario B: Continued Decline Through 2027

In the baseline scenario, nothing changes legislatively. Insurers finalize 2027 premium increases in the 14 percent median range. Another wave of moderate-income enrollees finds the math impossible. Enrollment falls to 17 or 16 million by late 2027. FQHC uncompensated care burden rises by an estimated $2.3 billion nationally based on NACHC projections. Safety-net hospital ED visits increase. State governments face pressure to expand their own subsidy programs, which most cannot afford.

This is the scenario that is already unfolding.

Scenario C: Market Exit in Key States

In the tail risk scenario, one or more major insurers exit the marketplace in high-loss states where the risk pool deterioration has been most severe. When an insurer exits a market, remaining enrollees face premium increases of 20 to 40 percent in a single year as the competitive price anchor disappears. Ohio, Oklahoma, and Arizona - which already saw 30 percent enrollment declines in 2026 - are the most vulnerable to this dynamic.

A market exit does not require insurers to do anything dramatic. They simply file a non-renewal with state regulators and let the contracts expire. The CMS Special Enrollment Period provisions cannot force coverage where no insurer is willing to price it.

6. The Nonprofit Hospital Question

One thread from the same KFF Health News piece that flagged the ACA enrollment crisis deserves its own attention: Congressional Democrats are now publicly questioning whether nonprofit hospitals are delivering enough community benefit to justify their tax-exempt status.

This is a legitimate question. The tax exemption for nonprofit hospitals is worth an estimated $28 billion per year nationally. In exchange, these institutions are supposed to provide charity care, community benefit programs, and services that advance public health. In practice, the amount of charity care varies enormously across institutions, and many nonprofit hospitals have moved toward revenue-maximizing behaviors that look very similar to their for-profit peers.

📊 The nonprofit hospital tax exemption is worth an estimated $28 billion per year nationally. IRS data shows charity care spending averages just 2.3% of operating expenses at many large nonprofit systems.

Here is the connection: you cannot ask hospitals to prove their community value while simultaneously cutting the insurance coverage of the communities they are supposed to serve. If 3 to 5 million people lose coverage and show up at nonprofit hospitals seeking charity care, the question of whether those hospitals are providing adequate community benefit becomes acutely relevant. A hospital that is genuinely fulfilling its community benefit mission should be seeing increased charity care spending in 2026. A hospital that is not is surfacing its own exposure.

Health system CFOs who are watching the nonprofit hospital scrutiny debate without connecting it to the ACA coverage losses are missing the story.

What This Means For You

The ACA enrollment collapse is not a policy abstraction. It has direct operational consequences for every institution in this newsletter's audience.

FQHC executives and CHC leaders: Your uninsured patient volume is rising now. Model your uncompensated care projections against the 3-million-loss baseline. If your Section 330 grant renewal is coming up in the next 18 months, document your uninsured patient surge with monthly data - this is exactly the evidence you need for grant justification and state advocacy.

Health system administrators and CMOs: Your emergency department is already seeing the early arrivals from the coverage collapse. Track ED visits by payer mix monthly through 2026 and 2027. The patients coming in uninsured today are the ones who had marketplace coverage last year. That is a quantifiable policy impact - use it in your state legislative engagement.

Radiologists and pulmonologists: The FQHC patient pipeline for lung cancer screening is under pressure. If your institution partners with FQHCs for CPT 0721T screening programs, ask your FQHC partners how their care coordinator staffing looks. A FQHC that cuts navigators to manage margin pressure will refer fewer patients to your program. Protect the navigator relationship proactively.

Healthcare investors and founders: The next 18 months will produce consolidation pressure on smaller FQHC networks that cannot sustain negative operating margins. Health system roll-up plays targeting FQHC networks in Ohio, Oklahoma, and Arizona will see motivated sellers. Separately, any company that can help FQHCs generate new revenue - 0721T screening programs, G0680 cardiac screening, remote monitoring - will find uniquely receptive audiences.

Policy advocates: The ACA comment and advocacy window is narrow. The 2027 rate filing deadline was July 15. If your organization has not submitted formal comments to your state insurance department on the proposed premium increases, that window is closing. The best evidence is patient-level testimony from people who have actually lost coverage - not aggregate statistics, but names and faces.

Closing

The ACA coverage collapse of 2026 is being narrated as a technical correction. It is not. It is the predictable consequence of removing price supports from a market where many buyers were already at the edge of affordability.

Congress made a deliberate choice to let the enhanced subsidies expire. Insurers made rational choices to raise premiums in response to a deteriorating risk pool. And millions of Americans made the only rational choice available to them: they stopped buying a product that no longer made economic sense for their households.

The institutions that will pay for that choice are the safety-net hospitals and FQHCs that cannot turn anyone away. They will absorb the cost in the form of uncompensated care that is rising faster than their grant funding, in the form of patients presenting later and sicker, and in the form of margins that are already negative and declining further.

The question for every health system leader reading this is not whether this will affect you. It already is. The question is how far you are into modeling the impact on your institution - and whether you have made the connection between a policy debate in Washington and the patients showing up at your door today.

What would it take for Congress to treat this as the public health emergency it is?

About the Author

Jonathan Govette is the Co-Founder and CEO of Oatmeal Health, an AI lung cancer diagnostic company catching cancers earlier in the communities that need it most. Oatmeal uses AI to identify unscreened high-risk patients, navigate them to care, and score every lung CT for malignancy risk - billed under CPT 0721T. Stage I survival is 77%. Stage IV is 9%. We work in FQHCs because that gap is largest there.

Jonathan writes daily about radiology, pulmonology, AI diagnostics, health policy, hospital operations, and healthcare startups.

Subscribe to stay ahead of healthcare's most important shifts. Weekly deep-dives on AI, radiology, health policy, FQHCs, and the business of healthcare - written for operators, clinicians, and investors who want the signal, not the noise. Subscribe at oatmealhealthjonathangovette.substack.com

Key References

KFF: ACA Marketplace Enrollment is Down in 2026 - https://www.kff.org/affordable-care-act/aca-marketplace-enrollment-is-down-in-2026-but-all-of-the-data-isnt-in-yet/

KFF: Average Marketplace Deductible Grew $1,000 in 2026 - https://www.kff.org/affordable-care-act/the-average-marketplace-deductible-grew-by-about-1000-per-person-in-2026-with-more-enrollees-shifting-to-higher-deductible-plans-as-enhanced-tax-credits-expired/

KFF: ACA Marketplace Insurers Propose 14% Premium Increase for 2027 - https://www.kff.org/affordable-care-act/in-preliminary-rate-filings-aca-marketplace-insurers-largely-propose-double-digit-premium-increase-for-2027-following-a-steep-climb-this-year/

CNBC: ACA Enrollment Falls as Enhanced Subsidies Lapse (July 3, 2026) - https://www.cnbc.com/2026/07/03/aca-enrollment-enhanced-subsidies-lapse-fraud.html

KFF Health News: The Politics of Health at Midyear (July 9, 2026) - https://kffhealthnews.org/podcast/what-the-health-454-democrats-midterms-nonprofit-hospitals-july-9-2026/